The Growth of Private Health Insurance in Asia

Transforming the Patient-Provider-Payer Triad

The article examines the rapidly expanding and increasingly important private health insurance market in Asia. Nearly 3 million Asians will actively seek health insurance by the end of 2020. Many Asian countries will experience a growing adoption of private insurance, including those with strong universal coverage. The increasing cost of healthcare and growing uncertainty is causing many consumers to invest in enhanced protection against healthcare-driven economic hardship. In response, insurance companies are introducing new products, technologies, and marketing strategies to help attract these consumers, including a more robust role for wellness-oriented approaches. This article considers the implications of this trend for the Asian healthcare ecosystem and offers recommendations for leveraging it to increase quality, affordability, and access.

The growth of the Asian private health insurance market is one of the most striking developments in the global healthcare ecosystem, and it is transforming the fundamental relationship between patients, providers, and insurers in many Asian countries. This development occurs against the backdrop of the massive and continually growing global healthcare market, which has reached US$12 trillion. Over the past two decades, the percentage of healthcare expenditure worldwide has increased two percentage points, from 8 per cent to just over 10 per cent. Moreover, the average global medical cost inflation rate is nearly 10 per cent, which is more than three times the general global rate of inflation. Nowhere is this trend felt more heavily than Asia, where the population exceeds 4.5 billion.

The private health insurance market in Asia is projected to continue expanding. Nearly 3 million Asians annually will actively seek health insurance by the end of 2020, and that number is projected to continue increasing. Many Asian countries will experience a growing adoption of private insurance, including those with strong universal coverage in places like Japan and Singapore. The increasing cost of healthcare is causing many consumers to invest in enhanced protection against healthcare-driven economic hardship. The recent and still evolving coronavirus crisis in Asia and globally is like to further accelerate the demand for increase health insurance. In response, insurance companies are introducing new products, technologies, and marketing strategies to help attract these consumers, including an enhanced role for wellness-oriented approaches. This article examines the implications of this trend for the Asian healthcare ecosystem and offers recommendations for leveraging it to increase quality, affordability, and access.

Several key Asian countries, including China and India, are experiencing a rapid increase in healthcare expenditures. The growth is primarily driven by the increased prevalence of chronic diseases, expanding healthcare awareness, surging geriatric populations, and proliferation of technology. There is an increased demand from both citizenry and governments in Asia for more accessible and sustainable health/medical/wellness service to the public. The region continues to be forecasted as one of the world’s fastest growing healthcare markets. Given the macro forces of economic development and population growth, health-related business investments in Asia are seen as having relatively little downside risk. One key area for investment is insurance. The market for individual insurance includes many components such as auto, long and short-term disability, health, home, and life. In this paper, we focus specifically on the Asian private health insurance market and how it is transforming the Patient-Provider-Payer triadic relationship between consumers/patients, hospitals/providers, and insurers/payers.

Four Fundamental Drivers

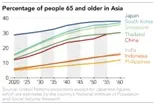

There are 4 fundamental dynamics driving changes in the Asian healthcare ecosystem as the populations become (i) older, (ii) wealthier, (iii) sicker, and (iv) more mobile. First, the proportion of citizens who are 65 and older is increasing and will continue to rise in most Asian countries (see Figure 1). For example, by 2025, the number of elderly in Indonesia will reach 45 million. By 2050, the elderly population in Vietnam is expected to quadruple from 2015 levels. The growing elderly population in Asia has generated more interest in early detection of key health issues like cancer, cardiovascular disease, and diabetes. Second, Asia has experienced significant expansion of wealth and a growing consumer middle class. In China and India combined, the number of middle-class households will soon exceed 200 million. Within the next five years, total household wealth in China, India, and the rest of Southeast Asia will surpass North America’s wealth. The Organisation for Economic Co-operation and Development (OECD) projects that by 2030, Asia will account for a remarkable 66 per cent of the global middle-class population and 59 per cent of total middle class consumption worldwide.

Figure 1:

Third, as the middle class in countries like China and India grows, there is a corresponding increase in the number of lifestyle diseases (e.g., diabetes, heart disease, obesity). Much of the increase in lifestyle diseases is driven by the adoption of a higher fat content Western diet and a shift to more sedentary life patterns. As citizens in Asian countries become older, richer, and fatter, this presents a unique opportunity for private insurance. In Asia, middle class consumer expenditures on the category of “health, beauty and wellness” is second only to the category of “travel and leisure.” The top five factors that most drive increases in medical care costs are metabolic/cardiovascular risk, occupational risk, environmental risk, dietary risk, and emotional/mental risk. There is a growing incidence of non-communicable diseases such as diabetes and obesity. Between 2012 and 2017, the number of dialysis patients in China doubled to reach over 450,000. By 2022, the number of dialysis patients is expected to exceed 800,000. In China alone, the market for dialysis-related services is increasing by 20 per cent per year and is predicted to exceed $7.5 billion by 2020.

Fourth, there is increased international mobility throughout Asia. Given the diversity of countries, as well as the flows of people across the region, the Asian market is both complex and varied. The high Asian population mobility includes expatriates and medical tourism. The rapidly increasing expats living in Asia includes (i) expatriates moving into economically thriving areas such as China, Hong Kong, and Singapore, (ii) Asia expatriates who move to areas such as the Americans, Europe, or the Middle East, (iii) medical tourists seeking higher quality and/or low cost care in countries such as India and Singapore, and (iii) Asia medical tourists who seek higher quality care primarily in Europe or the United States. These shifting regional migratory patterns impact the provision of healthcare and hence the utilisationof health insurance. These work-related mobility patterns of expatriates, both those into (e.g., shifts to China, Hong Kong, Singapore) and those out of the region (e.g., shifts to the Americas, Europe, or the Middle East), are an important consideration regarding health insurance. Given its rapidly growing and globally mobile populations, Asia is now a high priority market for many international health insurers. Globally, mobile people are a primary target for private medical insurance providers. There is an increasing demand for insurance that will cover people across the broader Asia territory as patients want to be able to access the best healthcare facilities and centers of excellence wherever they are in Asia.

Trends in Asia Healthcare Market

The global healthcare insurance market is expected to reach $2.2 trillion by 2024, and the Asia-Pacific market is expected to account for almost $500 billion of this total –nearly 1/4th. Asia includes a diverse mix of markets/nations, including the huge markets (mainland China and India), mature markets (e.g., Australia, Japan, South Korea), developing markets (e.g., Indonesia and Vietnam), and hybrid markets (e.g., Hong Kong and Singapore). The Asia-Pacific healthcare sector is one of the world’s fastest growing at 19.9 per cent, according to one estimate. As noted earlier, one contributor to this is the rapidly expanding industry for non-Asians visiting Asia for medical care. The global medical tourism market is approaching US$20M annually and is estimated to generate revenue of nearly US$30B by 2025. The Asia-Pacific region is leading in the growing medical tourism medical market. Medical tourism accounts for more than 30 per cent of revenue in Southeast Asian private hospital revenue. Given the multiple regional centers of excellence for healthcare in Asia, medical tourism is becoming increasingly important.

Success in the complex and diverse Asia-Pacific market requires a deep understanding of medical social, and technological dynamics. Key industry trends for the Asian healthcare industry include rising need for private insurance, increasing use of digital platforms in clinical trials, value-based reimbursement, and growth of home health monitoring platforms. The movement to outcome and value-based payments, which is now spreading rapidly in Europe and the US, is largely absent in Asia, but this will change. Value-based reimbursement models will soon have greater utilisation in Asia. Private and public payers are beginning to introduce outcome-based reimbursement models for expensive therapeutic care. Specific challenges for the healthcare ecosystem include the development of patient-focused technology platforms, a more empowered role of consumers in healthcare, and the need for policy innovation.

A more specific example of the many exciting developments unfolding across the Asian healthcare landscape is the substantial growth of “internet hospitals” in China. Last year, the Chinese National Health Commission issued a report indicating that there are currently 158 ‘internet hospitals’ nationwide. These innovative institutions allow patients to easily log into a hospital’s official account or software application for a video consultation with a healthcare clinician. Physicians are allowed to issue an immediate prescription if necessary. Major cities and provinces continue to actively launch new internet hospital outlets, but these do face challenges, including harmonising with the Yi Bao system, developing relationships with traditional hospitals, and finding a sustainable profit model. Private insurance is viewed as the ultimate companion for the ‘internet hospital’ business model. There will be increased cooperation between insurance companies and ‘internet hospitals.’ Additionally, life insurers (e.g., Qianhai Life in China) are also investing and building hospitals and nursing homes.

Growth in Asian Health Insurance

The expanding Asian healthcare market has given rise to a new and growing Asian private healthcare insurance sector. Consumers want to hedge their risk against healthcare-driven poverty. The rapidly increasing cost of healthcare services is motivating consumers to invest in stronger protection against healthcare-driven economic catastrophe in their family and personal finances. For example, in Malaysia, publicly funded health care is not widespread. Typically, Malaysians pay for their medical care using private insurance. Even countries with strong universal coverage systems in place --like Japan and Singapore-- are seeing increased demand for private health insurance.

As health insurance plans become increasingly popular in Asia, the industry is producing several advancements and innovations. Asia is beginning to sprout Fintech and Insurtech unicorn companies focused on the private health insurance market. “Health insurance is the new growth engine for insurance in China,” explained Sebastien Gaudin, CEO of CareVoice, an Insurtech company operating in China. In China, private healthcare and private health insurance are still relatively novel markets. Deregulation in China, India, and other key markets has lessened barriers to foreign ownership, creating new opportunities for multinational insurers. The percentage of private health insurance spend remains relatively small at only 2 per cent of the total global healthcare expenditure. While Asia does offer huge opportunities for health insurers, the rules of engagement are rapidly changing.

The growing demand for healthcare insurance has not been satisfied by the supply. As a result, consumers in Asian countries are significantly underinsured. Zurich-based insurance company Swiss Re defines the “health protection gap” as “the sum of financial stress arising from unforeseen, direct, out-of-pocket medical expenses and the unaffordable portion that households avoid”. The total health protection gap in emerging markets is estimated to be US$310 billion or 1 per cent of the aggregate gross domestic product of these countries. In 2017, this health protection gap in Asia reached US$1.8 trillion, impacting over 40 million households. This gap is expected to widen in the coming years. In comparison to other parts of the world, Asia is especially vulnerable regarding health and life insurance protection gaps. Reducing the protection gap will require a collaboration of government and private insurers.

In comparison, North America is currently the leading global healthcare insurance market. The U.S. has a well-structured insurance and healthcare system as well as a compulsory provision of health insurance by employers. In the US, commercial insurance covers over 40 per cent of the nation’s total medical expenditures. In contrast, Chinese private health insurance covers only 1.4 per cent of total medical expenses with the remainder being covered by basic universal medical insurance, Yi Bao. Healthcare funding is one of the most significant societal challenges today, and the private insurance industry can play a significant role in addressing this challenge. Out-of-pocket spending is stressful for individuals and families, and it can be financially catastrophic. The two megatrends of an aging population and an emerging prosperous middle class are putting pressure on governments to keep pace with the population’s growing demand for accessible, affordable, and high-quality healthcare.

In Asia, as with most parts of the world, government regulators have a significant impact regarding the provision of healthcare and health insurance, helping shape business tactics and insurance markets. For example, changes in a country’s regulatory structure could have the profound impact of shifting the burden of healthcare provision from the private to the public sector (or from public to private), which can substantially alter a region’s health insurance landscape. The influence of regulators varies among Asian countries, and public healthcare reforms are rapidly increasing the private sector healthcare ecosystem. Health insurers must strive to have a commercially viable business that is also fully compliant with laws and regulations. As the insurance market matures, insurers will needto achieve full compliance with the different regulatory environments and adapt to frequent changes. Insurers operating in the ‘grey area’ of the insurance market will have considerably less leeway as regulation tightens.

Understanding Asian Insurance Consumers

Consumers in many regions of Asia are wanting insurance companies to provide an ecosystem of services, including primary care, specialists, drugs/medicines, healthy living advice, and personal health records. Particularly among the younger generation, Asian customers want to select, manage, and utilise their health insurance in the same way they do with financial products such as bank accounts and credit cards. Even more important than pricing, the degree of comprehensiveness and flexibility is valued by customers. Consumers want enhanced control, a streamlined mobile enrollment experience, and a user-friendly interface, as well as online doctor consultations, a one-stop e-claim portal, and wearables. Insurance companies are shifting from being mere claims payers to being true health partners. Insurance providers are adding wellness services to the core insurance products as there is an increasing focus on helping members manage their own health, especially in terms of prevention. There is an increasing development of hybrid products that combine health insurance and long-term care. Also, the goal of many private insurers is to pay claims directly to medical institutions and cooperative pharmacies, thereby saving policyholders the expense and inconvenience of making advance payments for their treatment.

Primary business objectives of insurers include medical cost control, proper risk pricing, product/service development, actuarially strengthening the pool of covered lives, and preventative healthcare. Insurers need to understand how demographics (e.g., aging populations), migratory patterns (e.g., more expatriates), and lifestyle changes (e.g., higher calorie diets) are impacting the healthcare landscape. Service and technology will remain critical to differentiation. The insurance industry will need to do a better job developing new products/services, educating customers, and maximising evolving distribution channels and then engrain the solutions deeper into the Asian market.

The healthcare insurance industry in Asia is changing as disruptive, innovative players (e.g., compare sites and Robo Advisor companies) enter the market with novel value-added services for customers. In China, there is a particular concern with cancer. Thus, there is a greater interest in cancer-focused insurance products, particularly for coverage on overseas treatment. China Life has launched a new insurance product in collaboration with the internationally renowned Mayo Clinic, allowingpatients to receive diagnosis and treatment from Mayo’s experts. The service includes express appointment making, remote consultation, itinerary arrangement for travel if needed, and unlimited follow-on sessions at Mayo.

There is an increased digital transformation and product innovation in the Asia insurance sector. The region has the highest smart-phone adoption rate in the world and a plethora of cloud-based infrastructures for storing, accessing, and sharing data. In Asia, digitalisation is transforming the strategic, operational, sales, and marketing dimensions of the health insurance industry. For some, it is digital disruption, but for others, it is digital enhancement. Insurance companies are aiming to capture the hearts and minds of younger generations (e.g., Millennials and Gen Z). The key is to engage users and enhance their experiences. Digital distribution is increasingly important. Younger people are accustomed to digital products and consume information differently. Digital savvy Millennials expect frictionless, hassle-free technology platforms that are personalised and can be securely accessed anytime, anywhere.

The other technology services being made available by insurers include artificial intelligence supported diagnostics, diabetes detection apps, employee assistance programs, and online doctor services. The new and long-standing technologies being leveraged include augmented intelligence, blockchain, chatbots, face/voice recognition technology, internet of things, machine learning, mobile apps, social media, and the cloud. Advanced data analytics are also allowing insurers to observe patterns and predict actions based on consumer histories and preferences. Insurers are increasingly able to anticipate consumer concerns. The goal is to make insurance more accessible and integrated into people’s routines. Data analytics provides real-time understanding of public responses to digital market campaigns, allowing for review and adaptation. Products also need to be made accessible to all levels of society.

Conclusion

The growth of the private healthcare insurance sector in Asia has important implications for economic growth and development across the entire region. Health insurance will become increasingly crucial to individuals, families, and communities. The COVID-19 pandemic has served to further heighted the appeal of and demand for supplement private healthcare insurance in Asia and elsewhere. Unlike general, life, or property insurance, health insurance is a product the user can (and should) actively engage. Unlike life insurance, which one hopes not to use, health insurance is often a service one should want to utilise (e.g., annual health checkup). The Asian insurance industry is reacting innovatively by encouraging the use of different health and wellness-related apps to promote healthy lifestyles, often leveraging gamification or rewards structures. Yet, given the growing number of new insurance providers, products, and services, there is a danger the consumers will be cognitively overloaded with choices and information. Historically, the health insurance sector has contributed to complexity rather than transparency, with an excess of opaque jargon. Consumers need enough information to make informed financial decisions and select the most appropriate insurance product. Thus, the industry will have to meet the challenge of remaining customer-centric. It will be fascinating to watch as the new Asian health insurance industry continues to grow and develop in these formative years, thereby fundamentally transforming the patient-provider-payer triad.

References:

https://www.prnewswire.com/news-releases/health-protection-gaps-in-emerging-markets---an-opportunity-for-health-insurers-to-serve-the-most-vulnerable-the-geneva-association-300814799.html

https://www.marsh.com/sg/insights/research/2019-medical-trends-around-the-world.html

https://www.un.org/development/desa/en/news/population/world-population-prospects-2019.html

https://www.quadriacapital.com, “Shaping Asia’s Healthcare for Tomorrow”

https://www.un.org/en/sections/issues-depth/ageing/

https://insuranceasianews.com/asia-pacifics-coming-insurance-boom/

https://insuranceasianews.com/asia-pacifics-coming-insurance-boom/

http://oecdobserver.org/news/fullstory.php/aid/3681/An_emerging_middle_class.html

https://www.marsh.com/sg/insights/research/2019-medical-trends-around-the-world.html

https://www.kidney.org/kidneydisease/global-facts-about-kidney-disease

https://www.businesswire.com/news/home/20190515005507/en/Healthcare-Insurance-2019---Global-Market-Size

https://sbr.com.sg/healthcare/asia/asia-hailed-worlds-fastest-growing-healthcare-market

https://www.ttgasia.com/2019/07/17/medical-tourism-generates-over-30-of-se-asian-private-hospital-revenue-new-report/

https://www.ttgasia.com/2019/07/17/medical-tourism-generates-over-30-of-se-asian-private-hospital-revenue-new-report/

https://www.mobihealthnews.com/news/asia-pacific/chinese-insurtech-startup-carevoice-lands-roughly-10m

https://www.prnewswire.com/news-releases/health-protection-gaps-in-emerging-markets---an-opportunity-for-health-insurers-to-serve-the-most-vulnerable-the-geneva-association-300814799.html

https://www.swissre.com/reinsurance/life-and-health/reinsurance/closing-asia-health-protection-gap.html

https://www.genevaassociation.org/research-topics/protection-gap/healthcare-emerging-markets-exploring-protection-gaps?utm_source=HPGemergingReport-PressRelease&utm_medium=media&utm_campaign=hpg+emerging+markets

https://www.marketing-interactive.com/the-building-blocks-of-wellbeing-new-frontiers-of-hong-kong-insurance-marketing/

https://www.asiainsurancereview.com/Magazine/ReadMagazineArticle?aid=42615

James Gillespie

Faculty Member, Department of Business and Economics, Saint Mary’s College

Linsey Feit

Healthcare Consultant, Optum

Addie Bobosky

Junior at Saint Mary’s College